Understanding the Differences Between Morabaha and Usury & The Benefits of Morabaha Financing in Islamic Finance

Morabaha and usury are two financial concepts that are often used in Islamic finance. While both involve the lending and borrowing of money, there are important differences between the two that it is important to understand.

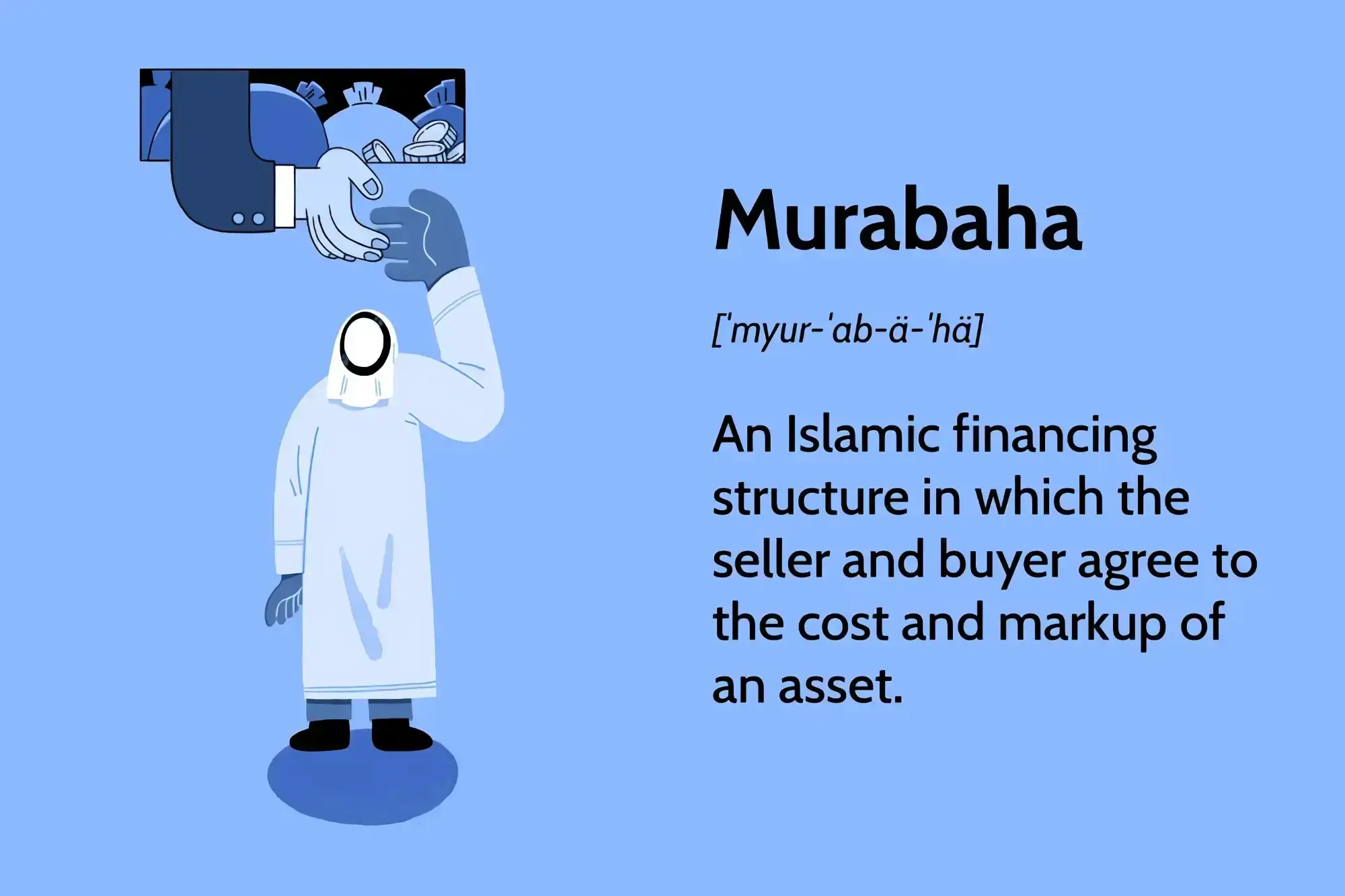

Morabaha, also known as cost-plus financing, is a form of financing that is allowed under Islamic law. In a morabaha transaction, the lender provides funds to the borrower to purchase a specific asset. The borrower then sells the asset to the lender at a profit, and the lender charges the borrower a fee for the financing provided. The profit earned by the lender in a morabaha transaction is called the mark-up, and it must be disclosed to the borrower at the time of the transaction.

Usury, on the other hand, is the practice of charging unreasonably high interest rates on loans. This practice is prohibited under Islamic law, as it is seen as exploitative and against the principles of justice and fairness.

One of the main differences between morabaha and usury is the way in which the profit is earned. In a morabaha transaction, the profit is earned through the sale of the asset, rather than through the charging of high interest rates. This means that the profit earned by the lender is linked to the performance of the asset, rather than being based on the borrower’s ability to pay.

Another key difference between the two is the level of risk involved. In a morabaha transaction, the risk is shared between the lender and the borrower. The lender assumes the risk of purchasing the asset, while the borrower assumes the risk of selling the asset. In usury, the risk is largely borne by the borrower, as they are required to pay high interest rates regardless of the performance of the asset.

There are several benefits to using morabaha as a form of financing, both for lenders and borrowers. For lenders, morabaha allows them to earn a profit while still complying with Islamic principles. It also allows them to diversify their investments, as they can invest in a range of different assets.

For borrowers, morabaha can be a more affordable and flexible alternative to traditional loans. Because the profit earned by the lender is linked to the performance of the asset, the borrower’s repayment obligations may be lower if the asset performs poorly. In addition, morabaha transactions can be structured in a way that allows for deferred payments, making them more accessible for borrowers who may not have the ability to make large upfront payments.

So resuming the benefits of Morabaha

- Morabaha allows lenders to earn a profit while still adhering to Islamic principles, as the profit is earned through the sale of the asset rather than through the charging of high interest rates.

- Morabaha allows lenders to diversify their investments, as they can invest in a range of different assets.

- Morabaha can be more affordable and flexible for borrowers, as the profit earned by the lender is linked to the performance of the asset and repayment obligations may be lower if the asset performs poorly.

- Morabaha transactions can be structured to allow for deferred payments, making them more accessible for borrowers who may not have the ability to make large upfront payments.

- Morabaha can provide a sense of security for both lenders and borrowers, as the asset serves as collateral for the loan.

- Morabaha can be a more transparent and predictable form of financing, as the mark-up must be disclosed to the borrower at the time of the transaction.

Overall, morabaha is a viable alternative to traditional loans that allows for the lending and borrowing of money while still adhering to Islamic principles. While it may not be suitable for all financial situations, it can provide a number of benefits for both lenders and borrowers in the right circumstances.